- Published on

Battle of the Neo Banks

- Authors

- Name

- AbnAsia.org

- @steven_n_t

Bill Gates once commented that: We always overestimate the change that will occur in the next two years & underestimate the change that will occur in the next ten.

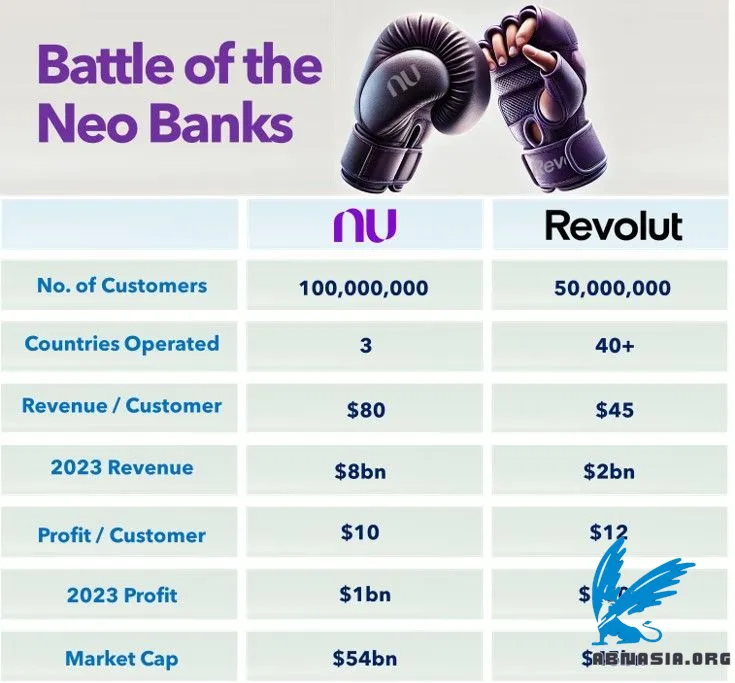

Nothing could be more true than what we are seeing about Fintech today. With challenger banks like Nubank & Revolut reportedly acquiring 100 and 50 million customers respectively, it is hard to argue that Fintech was just a fad. Within the well-known Gartner hype cycle these neo-challenger banks have long exited the “trough of disillusionment” and are now on the steepest trajectory on the “slope of enlightenment”.

Only a few years ago, there were many that asserted that Fintech was dead – given the tsunami of covid induced Fintech failures, but if there is one thing that is true, it is that if your going to do something disruptive, then do it right - digital lipstick will just not cut it. These neo banks appear to be a few of those that are getting it right, and we are witnessing in real-time all the 2010-14 prophecies about eating incumbent pie.

What is also interesting is that established banks are well aware that Rome is burning & many are now seriously investing in building a new challenger bank to rival or even cannibalize their existing proposition, or doubling down on efforts to transform the current digital services they offer. The lipstick is being replaced with a full face lift! The million dollar question however is can you take an established bank and transform it so that it can compete equally with a challenger bank like Nubank or Revolut? To do that, you need more than just a revamp of your digital services, you need a new culture, new ways of working and a technology infrastructure that is fit for purpose. You may even need new leadership on the board – the type that aren’t interested in short term PR, but rather systemic change in an era where technology advance is exponential.

So with that in mind, consider the definitions of what a ‘digital wallet’, ‘neo bank’, ‘challenger bank’ or ‘digital bank’ are? When does a wallet become a neo bank? Is it when it has a banking license, or is it when it adds lending to it’s portfolio of products and services? When does a ‘neo bank’ just become a ‘bank’? Is it when it has a lot of customers, or is there some better KPI? …and finally can a bank become a neo bank? Is it when it closes all it’s branches or is it allowed to have a few (or just one!?). What is a challenger bank? Is it a small startup, or can it be a bank launched by a bank to do things better because it can have a new set of rules and not inherit the established ‘baggage’ or ‘legacy’ that makes organizations lack agility & nimbleness? Soo many questions….

Banking and fintech is truly a fascinating industry at the moment and with the rapid rise of AI, WEB3 and maybe even a DAO based banking-as-an-algorithm organization there is clearly room for the next wave of challengers to the Nubank’s & Revolut’s of the world.

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA