- Published on

Mastercard Merchant Presented QR

- Authors

- Name

- AbnAsia.org

- @steven_n_t

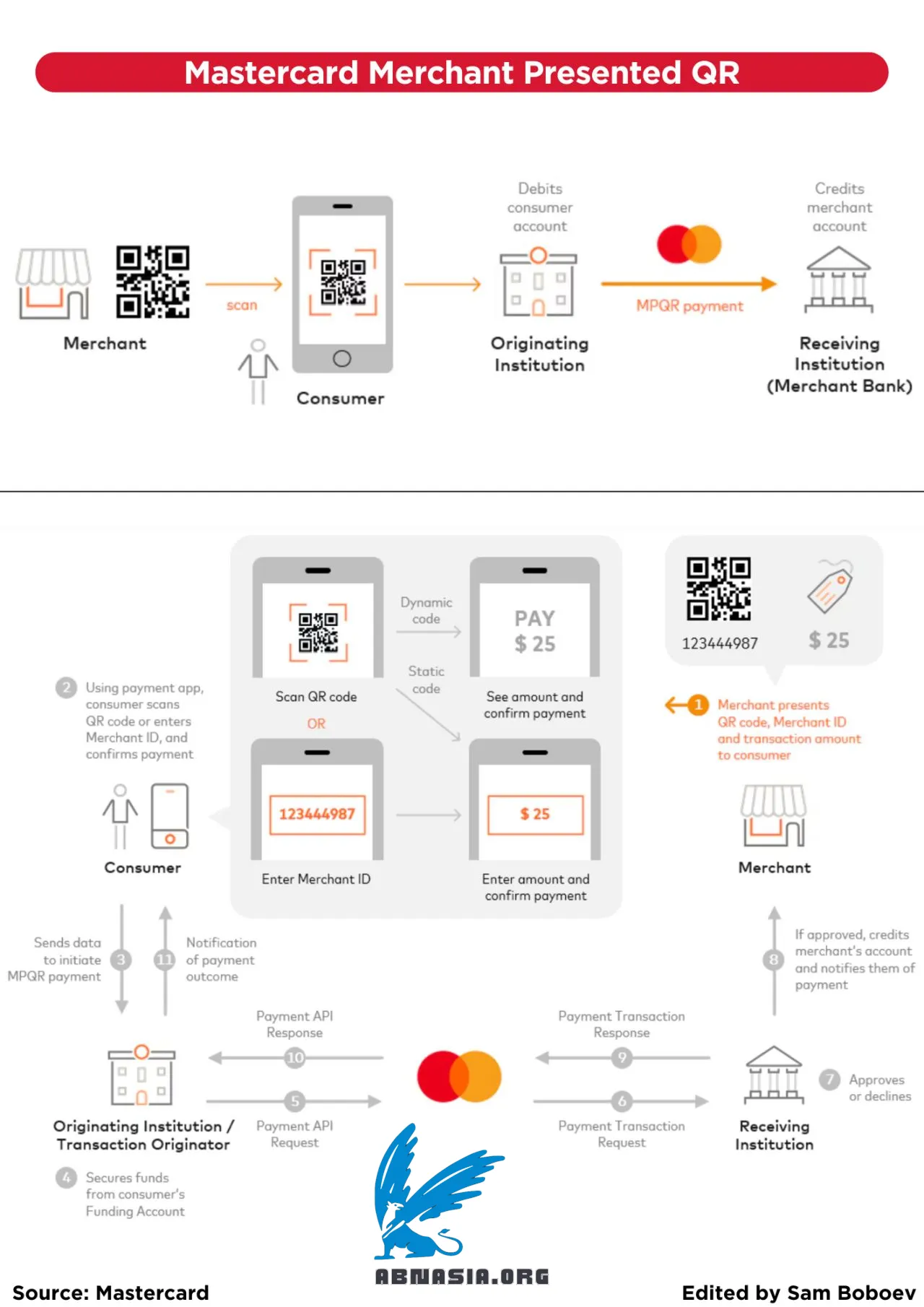

Mastercard Merchant Presented QR (MPQR) is a Mastercard QR program providing a consumer-initiated, mobile payment solution.

MPQR enables consumers to make cashless payments for goods and services from their mobile phones by simply scanning a Mastercard QR Code or manually inputting an alias provided by any Mastercard QR accepting merchant.

The MPQR program provides the SDKs, APIs and processing that enable registered participants to provide this payment solution:

Merchant banks (Receiving Institutions) can generate Mastercard QR codes for their merchants to present to their consumers.

Consumer banks (Originating Institutions) and wallet providers (Transaction Originators) can add Mastercard QR-scanning functionality to their payment applications (apps), enabling consumers to initiate MPQR payments when they scan merchants’ QR codes.

👉 How It Works

Merchants can present QR codes on their websites, mobile devices, in-store signage, invoices, ticket machines, and so on, providing additional secure payment methods to consumers.

🔹 The merchant (Recipient) presents their Mastercard QR code, Merchant ID (or Alias*) and transaction amount to the consumer.

🔹 These could be shown on the merchant’s website, mobile device, in-store signage, invoice, and so on.

🔹 Using a payment app, the consumer (Sender) scans the QR code or enters the Merchant ID/Alias (if unable to scan). The app parses and verifies the QR code and, if the QR code is dynamic, shows the amount to the consumer for confirmation. Otherwise, the consumer enters the amount and confirms payment.

🔹 The payment app sends the data to the Originating Institution/Transaction Originator to initiate the MPQR payment.

🔹 The Originating Institution/Transaction Originator verifies that the funding is available. If it’s the consumer’s bank, it debits the consumer’s account (Funding Account).

🔹 The Originating Institution/Transaction Originator sends a Payment API Request to Mastercard.

🔹 Mastercard sends a Payment Transaction Request to the Network to route to the Receiving Institution (Merchant Bank) for approval.

🔹 The Receiving Institution approves or declines the payment.

🔹 If approved, the Receiving Institution credits the merchant’s account (Receiving Account) and notifies them of the payment.

🔹 The Receiving Institution sends a Payment Transaction Response to Mastercard.

🔹 Mastercard sends a Payment API Response to the Originating Institution/Transaction Originator.

🔹 The Originating Institution/Transaction Originator notifies the consumer of the payment outcome via the payment app. If the MPQR Payment was rejected or declined, the Originating Institution/Transaction Originator must refund the Funding Account (if it’s the consumer’s bank).

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA