- Published on

Visa wants to become a network of networks. Re-inventing the card is a means to do it. Can they pull it off? Let's take a look.

- Authors

- Name

- AbnAsia.org

- @steven_n_t

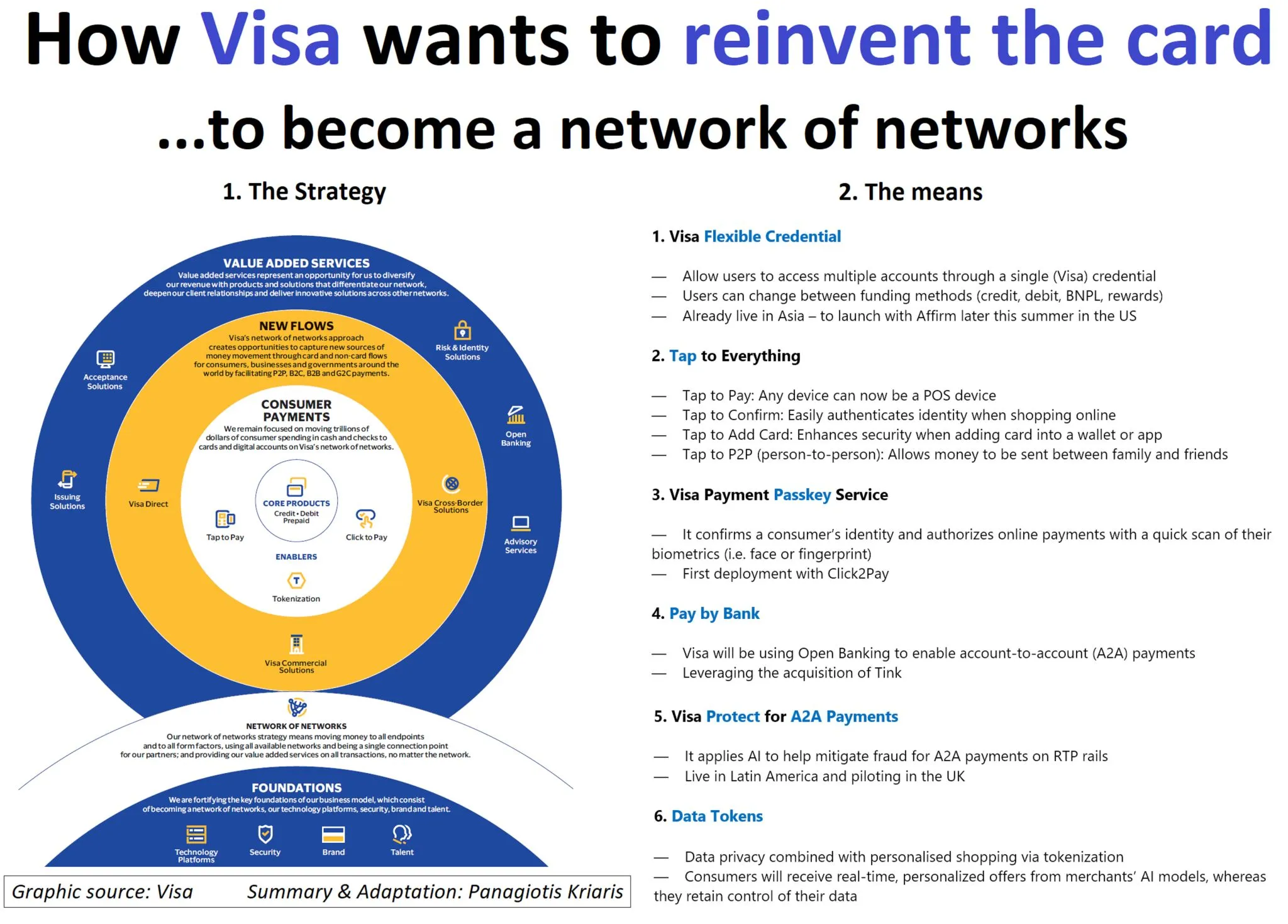

"On May 15th Visa announced a set of features aimed at revolutionizing the card. This is a summary:

- Visa Flexible Credential

Allow users to access multiple accounts through a single (Visa) credential

Example: Users can change between funding methods (debit, credit, BNPL, rewards points) and/or set preferences on their (mobile-banking) apps on when and how these will apply

Already live in Asia - to launch with Affirm later this summer in the US

- Tap to Everything

Tap to Pay: Any device can now be a POS device

Tap to Confirm: Easily authenticates identity when shopping online

Tap to Add Card: Enhances security when adding card into a wallet or app

Tap to P2P (person-to-person): Allows money to be sent between family and friends

- Visa Payment Passkey Service

It confirms a consumer's identity and authorizes online payments with a quick scan of their biometrics (i.e. face or fingerprint)

When shopping online, Visa passkeys replace the need for passwords or one-time codes, enabling more streamlined, secure transactions

As its first deployment of passkeys, Visa is integrating the service into Click2Pay

- Pay by Bank

Visa will be using Open Banking to enable account-to-account (A2A) payments

Leveraging the acquisition of Tink, Visa expands now the functionality from Europe to the US

- Visa Protect for A2A Payments

Aiming at solving one of the biggest challenges that the adoption of Real-Time Payments brings about: fraud

It applies AI to help mitigate fraud for A2A payments on RTP rails

Live in Latin America and piloting in the UK

- Data Tokens

Data privacy combined with personalised shopping via tokenization

Consumers will receive real-time, personalized offers from merchants' AI models, whereas they retain control of their data

These are not one-off features but have been years in the making and align with a long-term strategy. Here's what's behind:

Visa wants to ride the GenAI wave that is taking ecommerce and payments by storm

Empowering personalized experiences

Visa takes center stage, whereas funding methods take a step back. It's all about Visa

Tokenization, Tap2Pay and Click2Pay become the enablers behind Visa core products (credit, debit, prepaid)

Rather than a threat, Open Banking is integrated in a multi-payments infrastructure, becoming part of the Visa value added services

A further step for Visa to leverage global digital wallet adoption. All of the new features are powering mobile apps and digital wallets

It's all about the user experience (i.e. Tap2Everything)

Interoperability, privacy and security combined

Giving merchants, banks and consumers more flexibility and choice while remaining the driving force behind

Writer: Panag "

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA