- Published on

Wallet apps: how do they work?

- Authors

- Name

- AbnAsia.org

- @steven_n_t

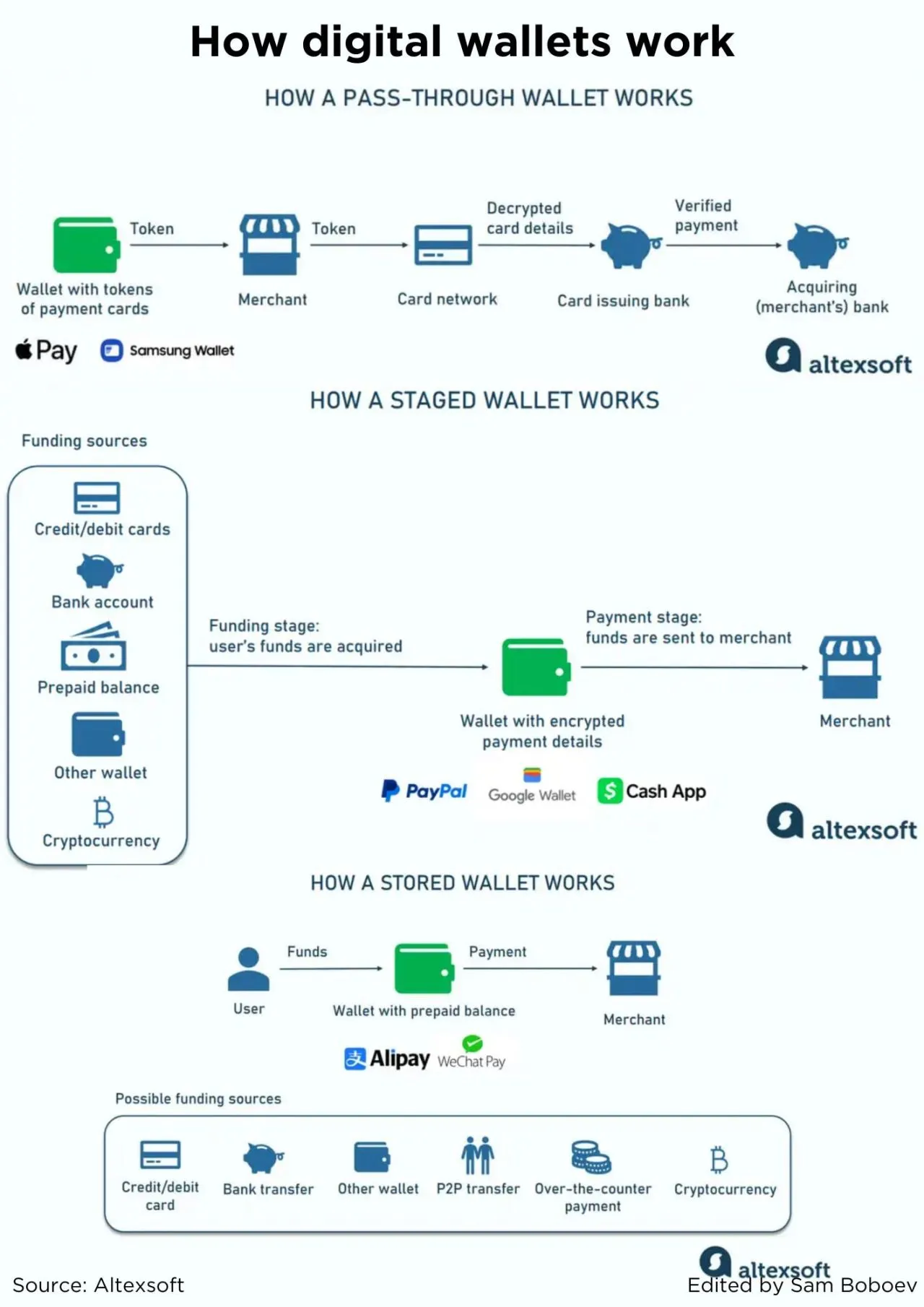

"Pass-through wallets, commonly designed as mobile-first, keep tokens that link to your credit and debit cards instead of storing sensitive data or money directly. They don't take part in moving funds. Once a transaction is initiated, such apps just pass encrypted information to a merchant - hence, the name.

In the course of further payment processing, the token travels to a payment network to be decrypted and checked against the actual card or account information in the issuing bank. After verification, the payment gets approved and sent to a merchant's acquiring bank. So, only the network and an issuing bank will know the actual card or account details.

Known for high security, pass-through wallets act essentially as extensions of credit and debit cards, so they are more widespread in regions with high card adoption, such as Europe and North America.

Major examples: Apple Pay, Samsung Wallet, Chase Mobile app

Staged wallets also house tokenized payment details but don't transmit them anywhere. Instead, they perform transactions in two stages. At the funding stage, the wallet acquires money from a customer's bank account, credit line, or other source. Then, at the payment stage, it sends funds to a merchant.

In this scenario, a wallet provider can make additional fraud assessments. At the same time, a payment network or card issuer may know nothing about details of a particular transaction that are disclosed during operations with pass-through solutions.

Staged options often support peer-to-peer transfers and cryptocurrencies and allow for storing funds right in the wallet's account.

Major examples: PayPal, Google Wallet (former Google Pay), Cash App (the US and UK only)

Stored digital wallets work as prepaid cards. Before making a transaction, a user must load money to a wallet's balance from a bank account, debit or credit card, via peer-to-peer transfer, etc. The availability of funding sources differs across providers, depending on the location and targeted users. A merchant withdraws money directly from the wallet.

Stored wallets are especially popular in unbanked and underbanked countries since they enable people to deposit money without having a bank account.

Major examples: Apple Cash (US only), Alipay (China's most popular e-wallet), WeChat Pay, Paytm Wallet (India's largest platform for instant payments).

Which wallet type and which brands, in particular, should travel companies care about in the first place? It largely depends on where their target audiences are."

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA