- Published on

AI and Its Precursors Are Not New To Fintech

- Authors

- Name

- AbnAsia.org

- @steven_n_t

Artificial intelligence and robotics are not new to financial services.

Artificial intelligence and robotics are not new to financial services. More so than most industries, financial services and especially payments, have relied on machines for decades to automate and accelerate transactions between people. Transaction authorization, credit underwriting, fraud detection, digital identities, and autonomous payments are all examples of machine-driven innovations that help us to transact on a daily basis more easily, securely, and effectively. While recognizing the decades-long technological journey to date, it is clear that AI is now pushing fintech beyond people-based dependencies. For example, fraud management models/machines are increasingly self-learning LLMs, not people-driven regression or rules-based models.

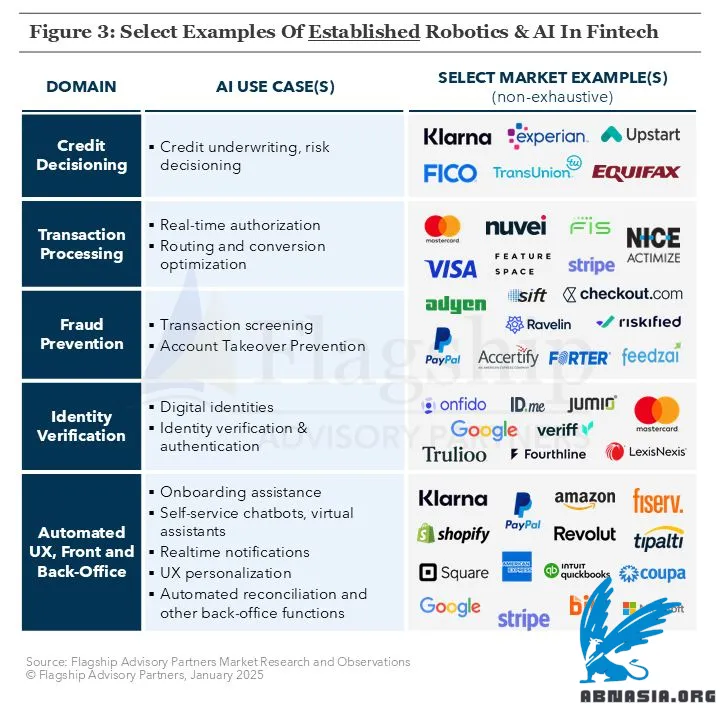

Below are examples where the usage of machine-/AI-driven decisions and robotics are well-established in the fintech industry today:

🔹 Credit decisioning: credit scoring and predictive models such as those offered by FICO have been around for decades, always evolving and improving. Underwriting processes that once took days are now done in real-time. Beyond the traditional scoring algorithms that are generally regression-trained on application and credit bureau data, AI (machine-learning) based underwriting models use broader, more comprehensive data inputs to find incremental lending opportunities.

🔹 Transaction decisioning: all payments involve payer and payee decisions to accept or deny the transaction, with a card authorization being a prominent example. Once a person presents an electronic payment, machines make these decisions and have for decades. Processors (merchant and bank) and networks now deploy AI models to optimize conversion while balancing potential fraud.

🔹 Fraud prevention and identity verification: paramount to making good transaction decisions, machines today recognize and validate our digital identities to avoid bad actors. Payment fraud detection is one of the most obvious examples of AI today. In parallel, forms of digital identities and technologies used to validate our identities continue to arise and evolve.

🔹 Automated servicing: servicing of financial services has migrated towards machine-based automation for many years, starting with the advent of banking chatbots in the mid/late 2010s. Self-servicing, real-time notifications, chatbots, and personalized web or app user experiences are all technologies that allow servicing without needing a person on the other end.

🔹 Orchestration and smart routing: machines are now working to improve your checkout experience and to ensure your payment requests are optimized as they travel through the complex value chain of payments.

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA