- Published on

Banking Model: Journey from Traditional Digital Banking to Open Banking and Data

- Authors

- Name

- AbnAsia.org

- @steven_n_t

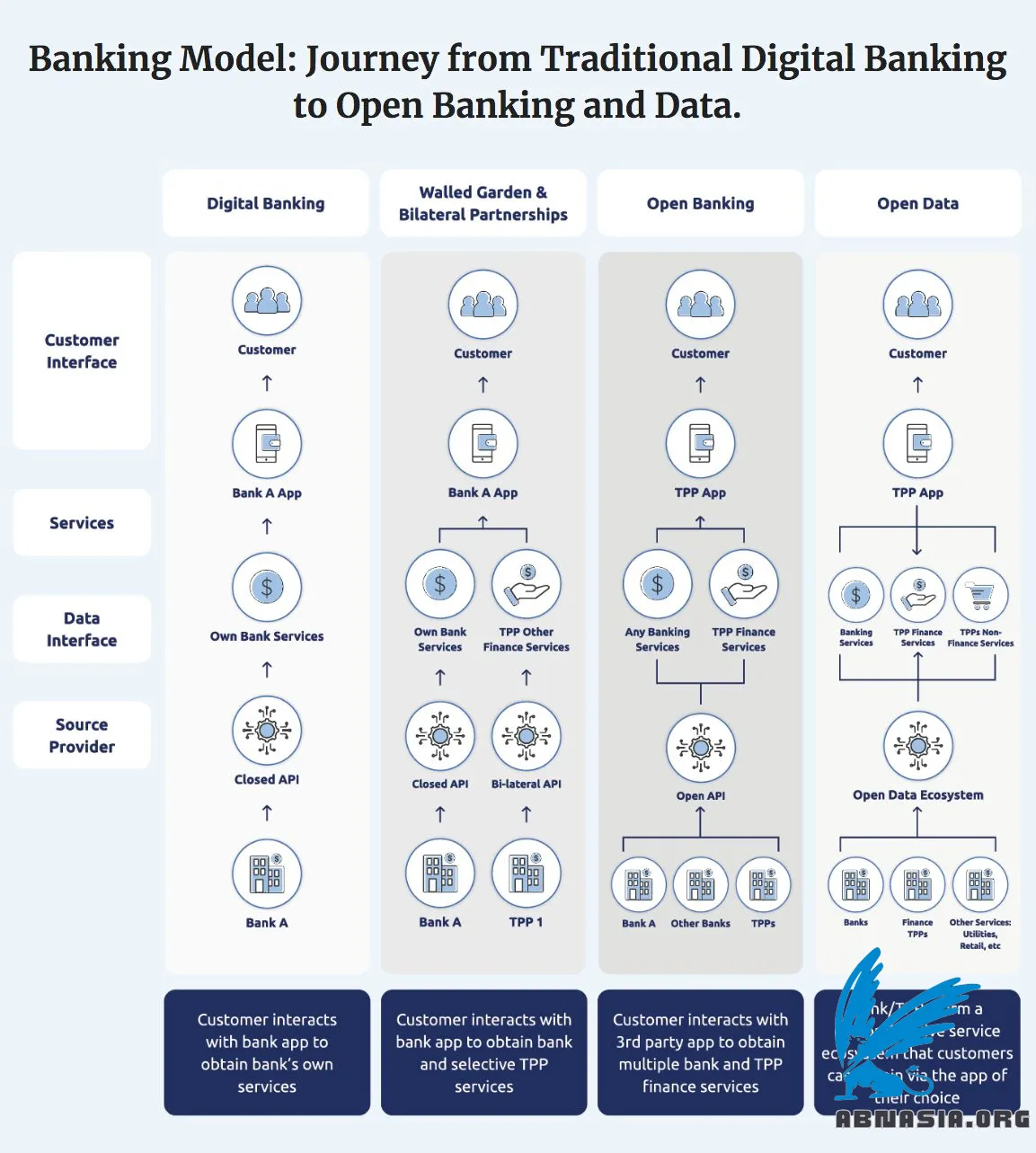

Fundamentally, open banking comes down to who owns data and how to use it. As data is more freely shared, new operating models have begun to emerge, allowing for the development of innovative services and new ways to deliver them to the customer.

Banking Model: Journey from Traditional Digital Banking to Open Banking and Data 💡

Fundamentally, open banking comes down to who owns data and how to use it. As data is more freely shared, new operating models have begun to emerge, allowing for the development of innovative services and new ways to deliver them to the customer 🙋♂️

Traditionally, banks have been the custodians of customer financial data. With open banking, customers can consent to securely share their data across multiple financial institutions with third parties.

Open banking does not preclude earlier operating models - banks can still offer dedicated apps within their own ecosystems for customers who do not consent to data sharing. Instead, open banking widens the scope of what is possible.

Open banking itself can be seen as an intermediate step towards what many executives refer to as open finance or open data. In a fully realized open data system, not only financial data but data across a multitude of sources - including utilities, government and others - can be securely aggregated into an innovative ecosystem. This allows for the provision of a wide range of services to customers and businesses, conveniently accessible via their preferred digital platform.

Four key steps in the open banking journey:

🔹 Digital Banking, with one bank providing its own digital banking services to its own customers.

🔹 Walled Garden, with one bank providing enhanced services including from third party providers (TPPs) all via its own customer app.

🔹 Open Banking, as data is more freely, customers access financial services from any bank or TPP via their preferred third party or bank app.

🔹 Open Data, whereby customers can now access financial as well as a wide range of other services provided by banks and TTPs via any third party or bank app.

These developments can have profound implications for banking strategies, both in terms of how they interact with customers and how customer data is managed. Their approach must consider how and whether they maintain control over the customer interface and position themselves in this new way of providing enhanced services digitally to customers.

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA