- Published on

Cross-border payments

- Authors

- Name

- AbnAsia.org

- @steven_n_t

Money transmitters vs Payment aggregation

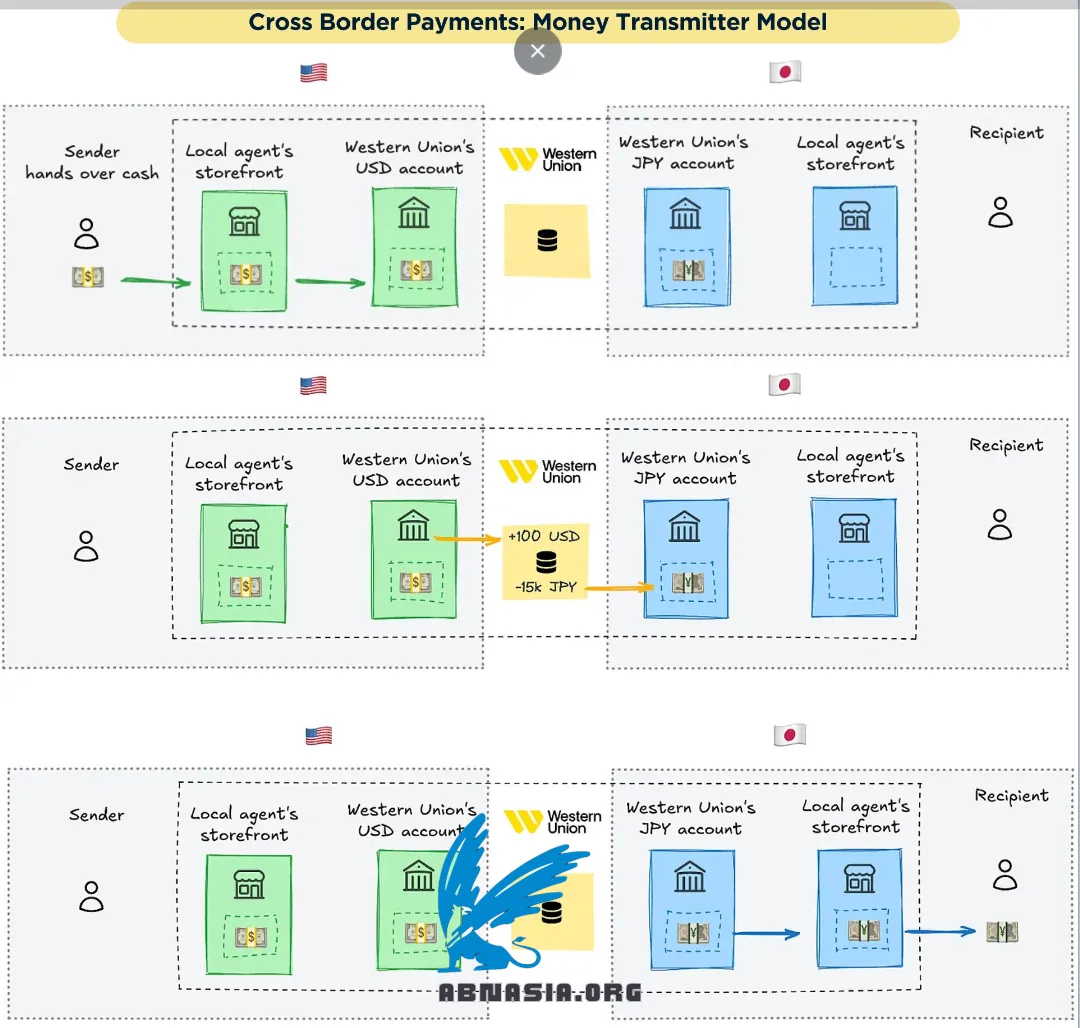

✅ Money transmitters

Money transmitters (MTs) such as Western Union and Moneygram are another long-standing and popular XBP method. They’re popular among the un/underbanked since the sender and/or receiver can transact in cash. MTs operate a global network of agents – physical storefronts such as conscience stores or currency exchange stalls – that offer MT services. Senders deposit cash with an agent and leave instructions for who can retrieve it elsewhere on the MT’s network.

For example, say I deposit $100 at a Western Union location in San Francisco and list my Japanese friend as the recipient. The agent verifies my request and then sends the funds to Western Union.

Western Union credits them to my friend in Japan and nets the funds between its USD and JPY accounts minus a fee. My friend can then pick up the equivalent in JPY at a Japanese Western Union agent by showing their ID or a confirmation code:

Correspondent banking and money transmitters are often critiqued for being slow and expensive. This cost and slowness are the downsides of their broad geographic coverage, resulting from their reliance on intermediaries. Because many MT users lack formal banking, an agent network is necessary for first/last mile distribution. In contrast, the lack of 1:1 global banking connectivity necessitates the correspondent banking network for the middle mile. Now let’s discuss two newer XBP models, which use technology to minimize intermediaries.

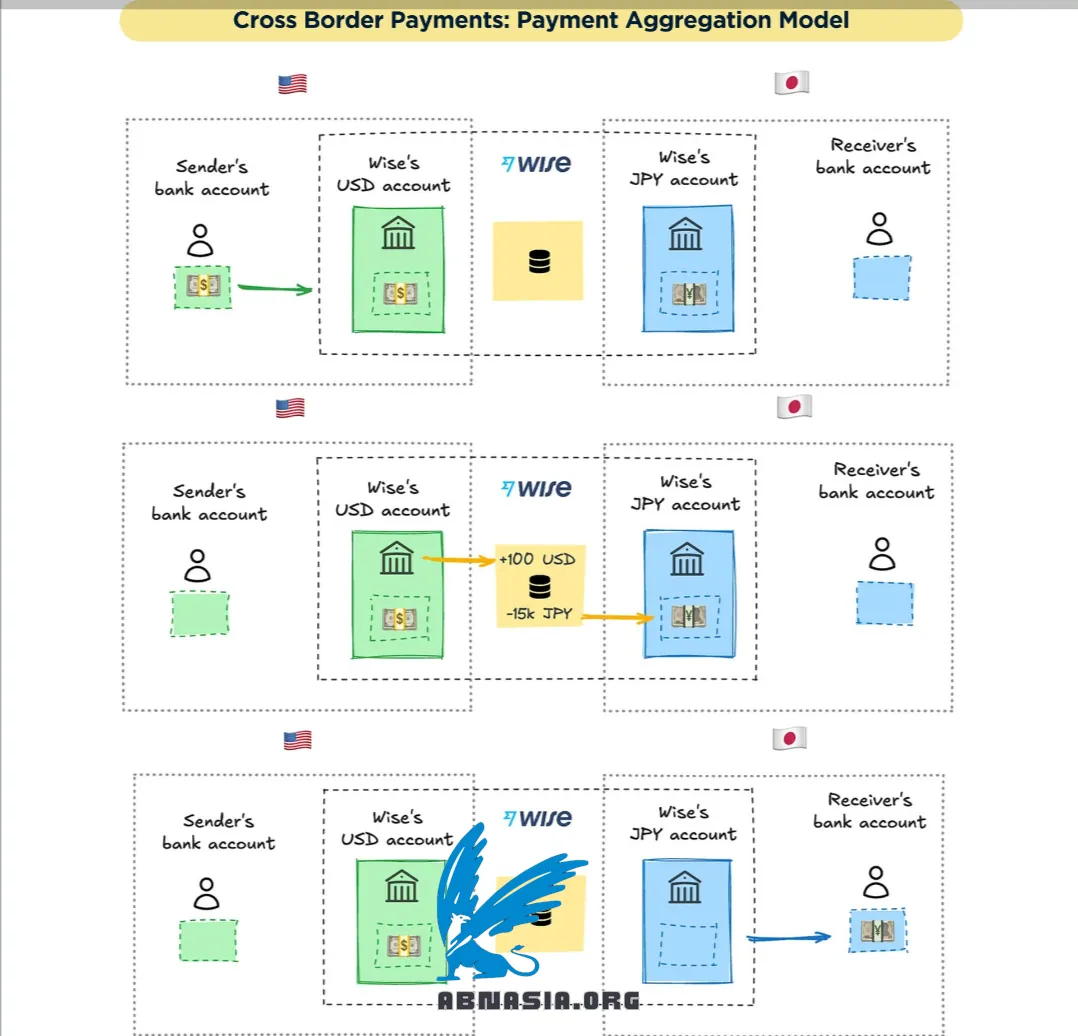

✅ Payment aggregation

Payment aggregators like Wise can be considered digital-first money transmitters, with apps instead of agent networks. These companies maintain bank accounts in the countries they support, pre-funded with local currency, and the infrastructure to pay in from and out to local users on each end. The actual “cross border” transactions are often internal net transfers, similar to correspondent banking, but the fintech orchestrates the transaction.

Let’s return to the example above, but use Wise to send money to Japan. Initiating the transfer, I’ll send $100 from my bank account to Wise’s USD account:

Wise will then transfer the equivalent amount from its JPY account in Japan to my friend’s SMBC account. No USD leaves the US and no JPY enters Japan.

This is faster and cheaper than correspondent banking and money transmitters because there are fewer intermediaries. Because Wise is the intermediary, it has more control over everything from the UX to the costs. This benefit does not come easily though. Beyond maintaining the local accounts, Wise must acquire and support users, comply with local regulations like KYC, manage liquidity and FX risk across countries, and more. Wise users are also limited to countries where Wise has established on/off ramps.

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA