- Published on

Greatest AI Potential in Banking

- Authors

- Name

- AbnAsia.org

- @steven_n_t

AI is becoming a make-or-break factor for banks. But success will not depend on their ability to offer AI, but on their competence in integrating it. Let's take a look.

Banking is forecasted to feel the biggest impact from generative AI among sectors and industries as a percentage of their revenues with the additional value calculated between 340 bn annually (source: McKinsey).

But why is the impact so powerful?

One of the main reasons is because the abrupt surge of gen AI is exponentially increasing the speed with which banking is being transformed.

That is not to say that the transformation has started with or due to AI. On the contrary: during the past 10 to 15 years banking was already in the middle of transforming from a human-based, relationship-first industry to a more automated and technology-driven business following the fintech revolution and the ascend of nimbler and more innovative competitors.

But AI now does 2 things:

It brings the transition to a new level, across 3 dimensions: speed, outcome and impact.

It turbo-charges one of the biggest challenges in modern FS: the combination of AI and data that brings under the same roof two inherently opposing forces: mass and customization. In other words, AI seems to find a credible answer to achieving hyper-personalization.

In a recent report Deloitte has provided realistic examples on how this is done across both cost efficiency and income growth:

Cost efficiency:

Workforce acceleration efficiencies across the board: 0-15% of total staff cost

IT development and maintenance acceleration: 10-20% of IT staff cost

Improved credit-risk assessment leading to 10-15% savings in impairment charges

Improved FinCrime/fraud detection reducing litigation/redress charges and fraud losses

Income growth:

Next generation market analysis / predictive trading algorithms: 5-7% uplift on trading income

Improved customer retention: 1-2% uplift on fees & commissions

Improved customer acquisition through hyper-personalised marketing: 5-10% uplift from interest income and fees & commissions

Tailored loan pricing based on credit risk assessment: 2-3% increase on net interest income

Despite all the excitement around these estimated benefits, success will not be a walk in the park. It will depend on the banks' ability to integrate AI in a seamless way into their day-to-day operations.

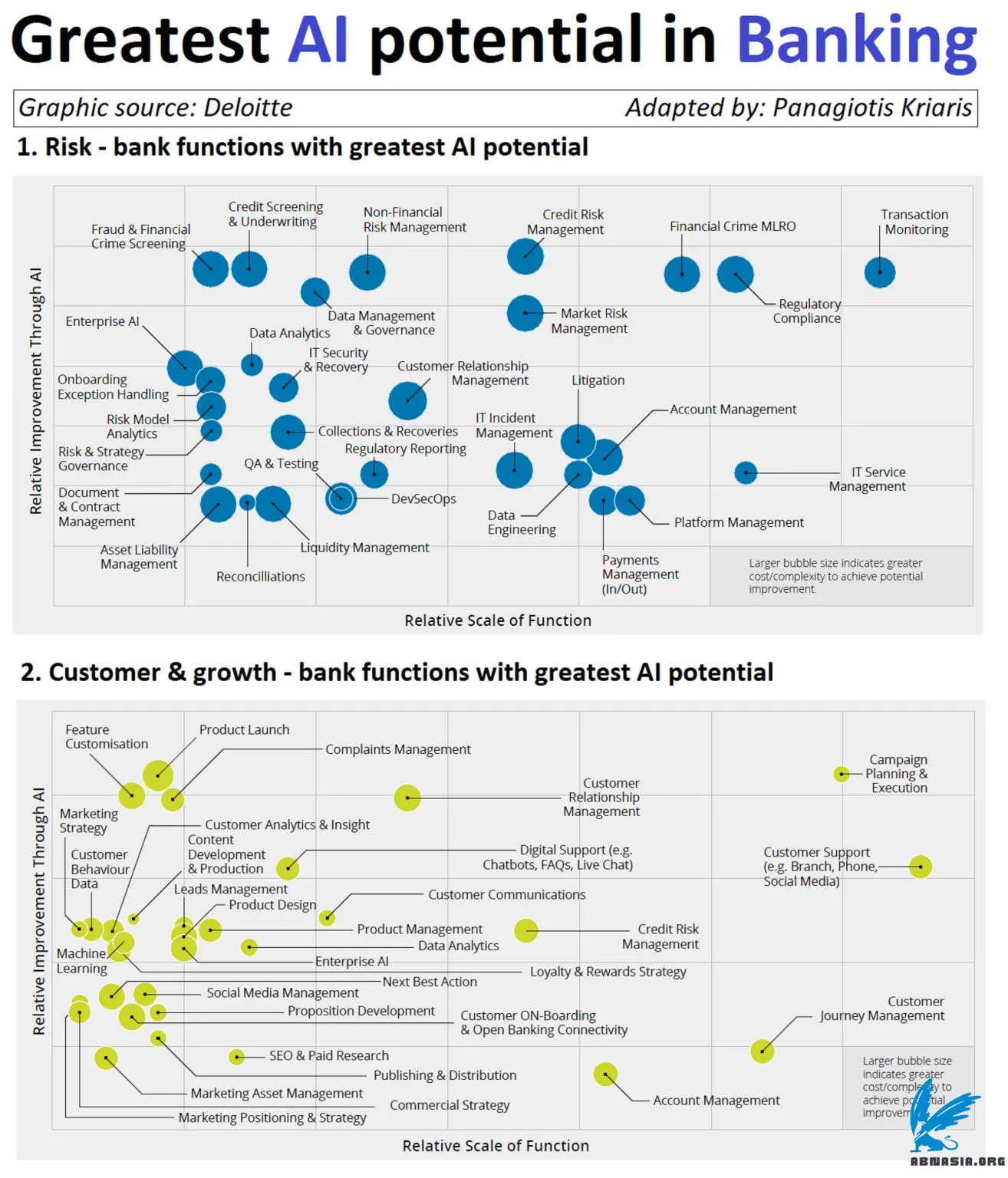

Going forward AI will be re-writing much of the scenarios and use cases of the banking value chain. That doesn't necessarily mean that they will all be different, but most will certainly be enhanced with impact spanning both across the back-end and the front-end. Given that resources are limited, one of the main challenges will be how to identify the ones to focus on. Factors such as strategy, potential impact and a match with the existing skillset should be guiding the selection process.

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA