- Published on

How does Mastercard Merchant QR Code replace PoS (Point of Sale)?

- Authors

- Name

- AbnAsia.org

- @steven_n_t

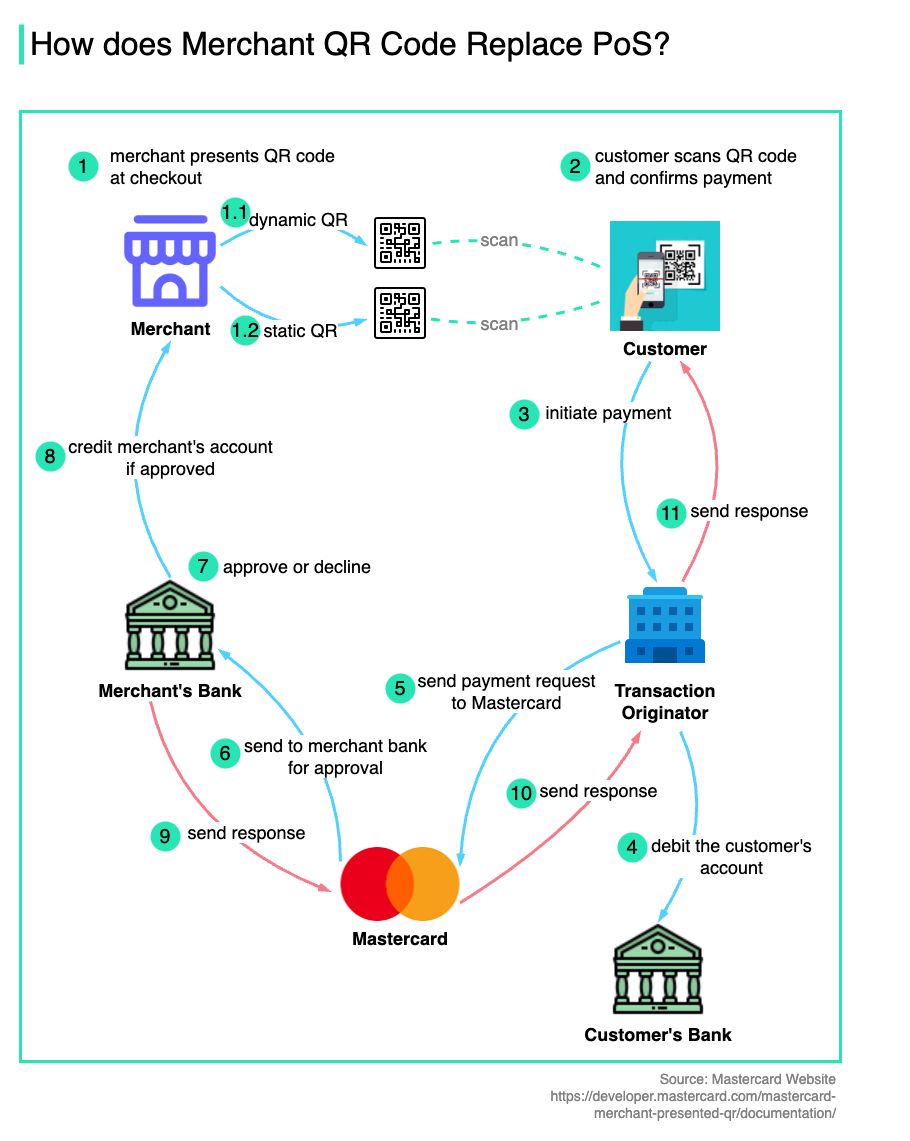

"The diagram below shows how Mastercard MPQR (Merchant Presented QR) works. There is no POS terminal or physical card involved.

🔹 Step 1: The merchant presents its QR code at checkout.

There are two types of QR codes:

Dynamic: the code is generated for each transaction and includes the payment amount

Static: the code is used for all transactions

🔹 Step 2: The customer scans the QR code using a mobile app and confirms the payment.

🔹 Step 3: The payment app sends transaction data to the transaction originator to initiate MPQR payment.

🔹 Step 4: The transaction originator debits the customer's account in the customer's bank.

🔹 Steps 5 and 6: The transaction originator sends a payment request to the Mastercard network. Mastercard routes the payment request to the merchant's bank.

🔹 Steps 7 and 8: The merchant's bank approves or declines the request. If it is approved, the merchant's bank credits the merchant's account.

🔹 Steps 9 - 11: The payment response is sent back all the way to the mobile app."

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA