- Published on

How Lending business is being redefined

- Authors

- Name

- AbnAsia.org

- @steven_n_t

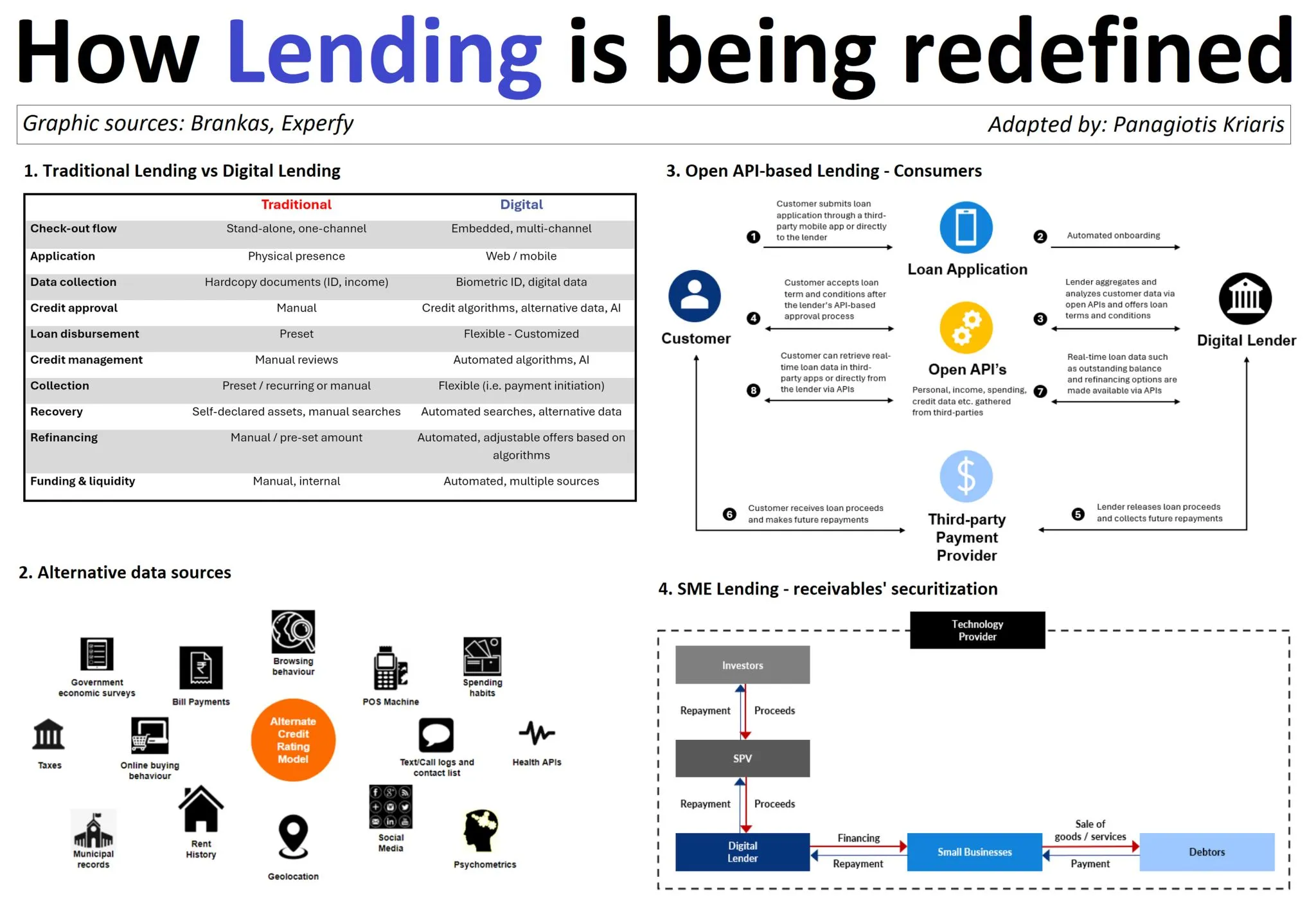

"There is no better way to understand the transformation of financial services (FS) than to look at how lending has - and is still being - redefined. Let's take a look.

Juxtapose a traditional mortgage or small business lending flow used to take weeks to decide and months to disburse vs the almost instant time-to-cash via an online platform and you have the epitome of the disruption that lending has gone through.

The main elements are:

A complete transformation of the end-to-end customer journey (from paper to digital and from an all-in to no human interaction).

From a stand-alone, vertical set-up handled exclusively by banks, lending nowadays finds itself at the convergence between platform models and cross-industry verticals managed by a plethora of players that can simultaneously act as both competitors and partners.

The addition of an entire level onto the front-end bringing non-traditional players into the game via what we call embedded finance: the art of adding FS flows in non-FS customer journeys.

Lending is about risk management and risk management is about data. Most of the innovation that has changed lending from the ground up evolves around the (right) handling of data: 1) Real-time, big data analytics 2) Algorithmic trading 3) Customer segmentation 4) Predictive analytics for fraud detection and lately 5) GenAI as a decision-making engine. At the same time 1) access to data has been democratized via open banking 2) rich, actionable data has replaced passive data 3) alternative data has redefined credit models.

The drive for hyper-personalized experiences via social commerce and the influence of algorithms and AI.

The re-packaging of existing financing flows into new business models via the help of technology. BNPL is a primary example.

My highlights include 2 conclusions to draw and 2 opportunities to consider.

Conclusions:

As more roles are concentrated under less layers, the dividing lines among lending, payments, e-commerce, fintech and banking are becoming less clear.

Lending remains at the epicenter of FS even for new players challenging the status quo. It is not by accident that the pivot of challenger banks to a mature 2.0. play goes through lending.

Opportunities:

Despite the digitization of the financing value chain, most new processes have been built around existing set-ups replicating models of a value chain that has dramatically changed. There is a significant opportunity in creating digital-native structures that can match new business models.

SME lending remains still one of the biggest, untapped opportunities in FS. Various approaches (from revenue-based financing to invoice discounting and to B2B PayLater) from different sides of the market (supply, operations, sales) are facing the same challenge: how to balance the inherent SME complexity with a higher degree of customization."

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA