- Published on

The Introduction to Cards in Payments by Travel & Payments 👇

- Authors

- Name

- AbnAsia.org

- @steven_n_t

The Key Players in Payments — Edition #2

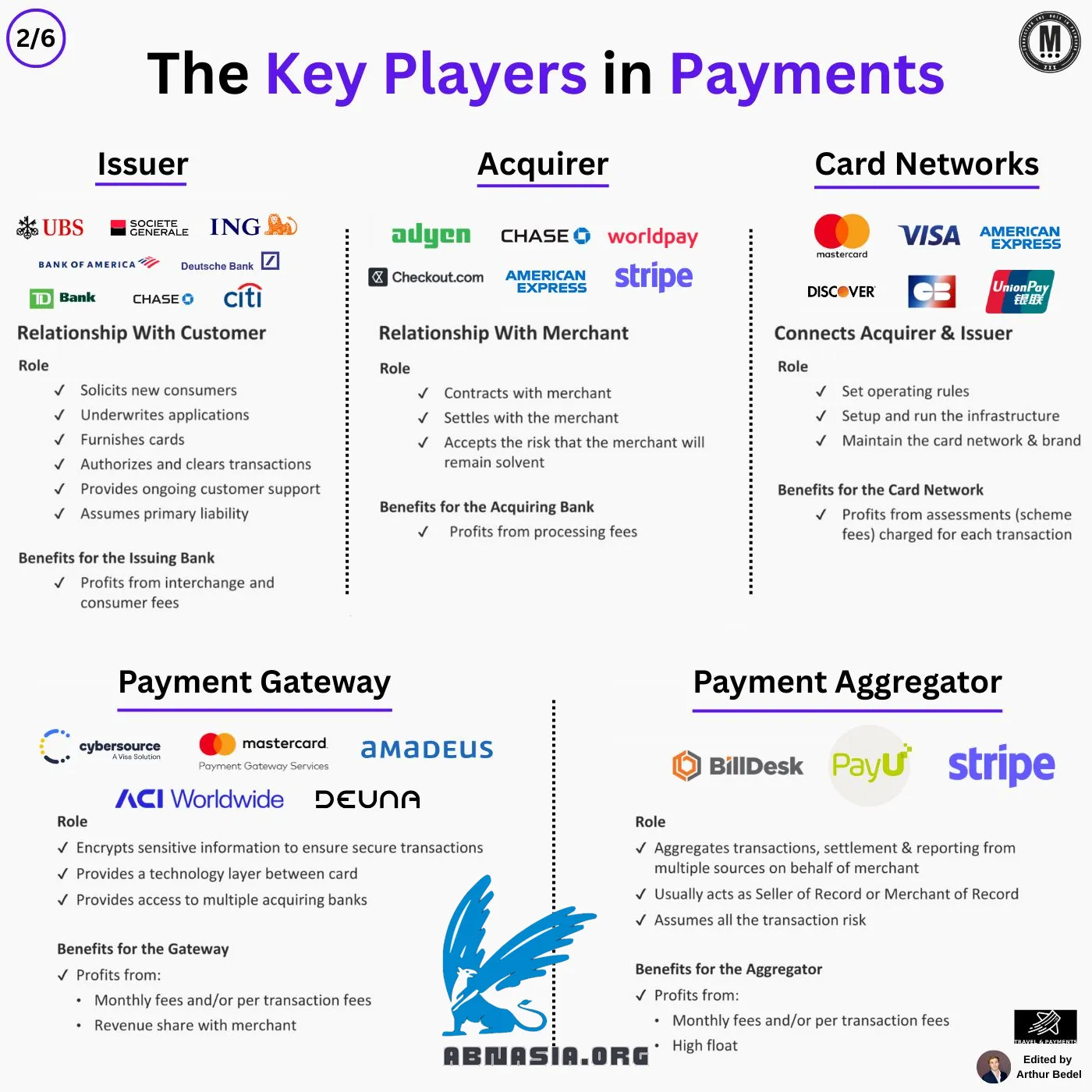

Behind every card transaction is a coordinated set of players — each with a unique role in enabling seamless, secure, and scalable payments.

—

Issuers: Issuers are banks or financial institutions that provide cards directly to consumers.

► Key Functions: → Underwrite and approve new cardholders → Furnish credit, debit, or prepaid cards → Authorize and clear transactions in real-time

► How They Make Money: From interchange fees, annual card fees, interest on revolving credit, and FX markups.

► Examples: Citi, UBS, ING, TD, Deutsche Bank, Chase

—

Acquirers Acquirers are responsible for enabling businesses to accept card payments.

► Key Functions: → Set up and manage merchant accounts → Process card transactions and settle funds to merchants → Manage chargebacks and fraud risk

► How They Make Money: Through processing fees, gateway charges, and often value-added services (fraud protection, analytics)

► Examples: Checkout.com, Worldpay, Nuvei

—

Card Networks Card networks serve as the central infrastructure layer between issuers and acquirers.

► Key Functions: → Route transaction requests between issuer and acquirer → Establish dispute resolution protocols → Set interchange and assessment fees → Manage card branding and acceptance standards

► How They Make Money: Card networks earn scheme fees, cross-border fees, and fraud assessment charges

► Examples: Visa, Mastercard, American Express, GIE Cartes Bancaires

—

Payment Gateways Gateways act as the secure portal through which card data travels from the consumer to the acquiring bank.

► Key Functions: → Route transactions to the appropriate processor → Offer tools for fraud prevention, 3DS, and retry logic → Provide dashboard and reconciliation interfaces to merchants

Note: The tokenization process may be performed by 3rd Party vault VGS, Acquirer Checkout.com, Gateway DEUNA, and Merchant...

► How They Make Money: Gateways charge monthly platform fees, per-transaction fees, and revenue-sharing arrangements

► Examples: DEUNA, CellPoint Digital, Amadeus

—

Payment Aggregators Aggregators combine payment services into a single offering, especially for smaller merchants

► Key Functions: → Act as Merchant of Record (MoR), processing under their own MID → Aggregate transactions across merchants → Handle onboarding, settlement, and risk management

► How They Make Money: Profit from higher per-transaction fees and managing float

► Examples: Paddle, Stripe, PayU, BillDesk

—

Next Up #3: The Payment Method Guide

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA