- Published on

The most crucial digital wallets battle

- Authors

- Name

- AbnAsia.org

- @steven_n_t

It has gone unnoticed, but the most crucial digital wallets battle is unfolding on the infrastructure level and has to do with interoperability. Let’s take a look.

Digital Wallets have become the number 1 payment method globally, with a forecasted 5.2 bn of users in 2026.

But while their popularity has surged, there are a few crucial gaps:

Unevenly distributed growth with most of the Digital Wallet success stories having either a local (mostly) or a regional focus.

Different payment preferences and varying technical capabilities translating to a de-facto fragmented landscape.

In effect, these gaps lead to a massive constraint:

Lack of interoperability.

Users of one Digital Wallet cannot communicate (send / receive funds) with those of another.

The gap is a huge one and it will only grow bigger. But so is the opportunity.

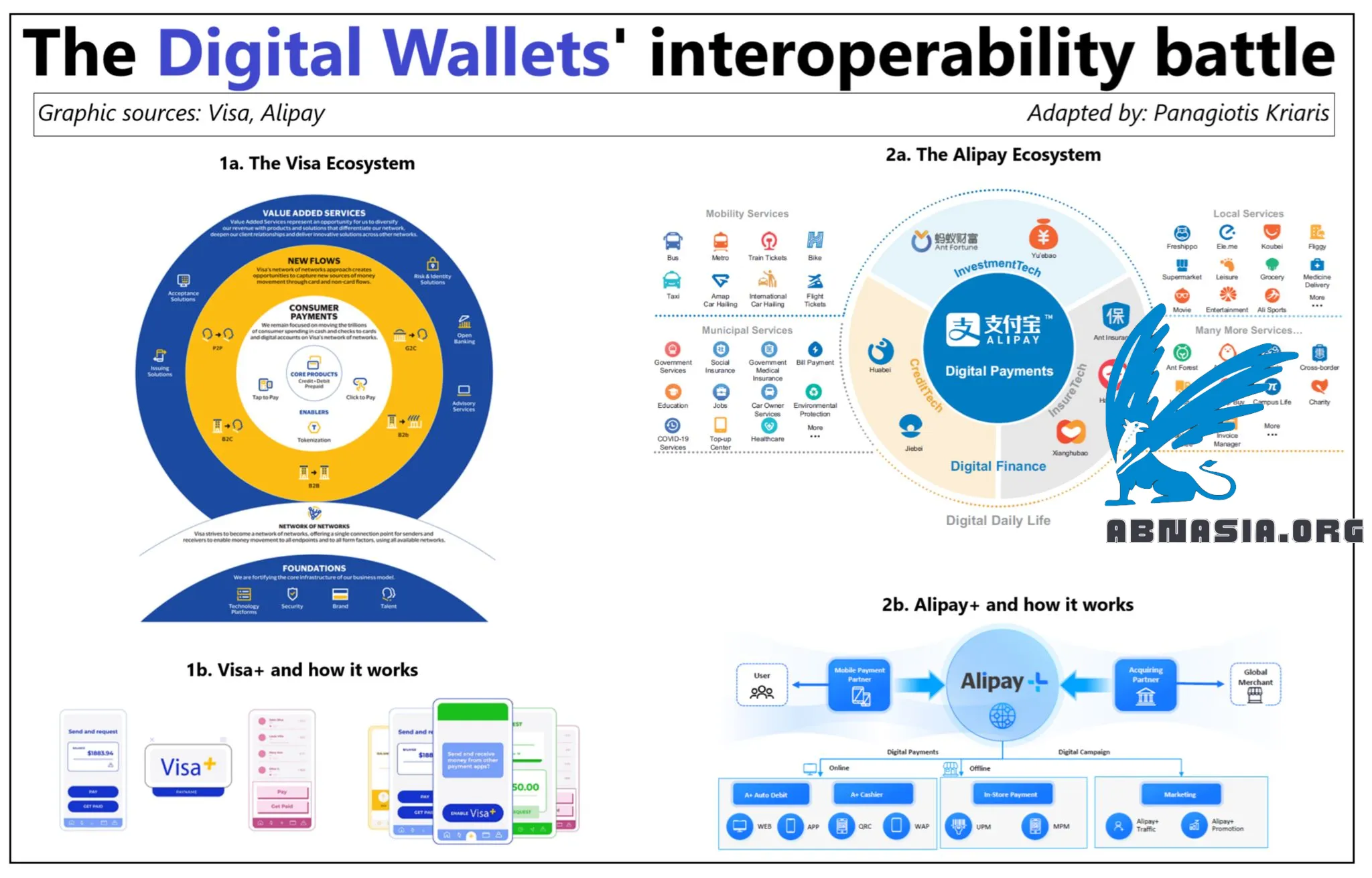

Two global players have identified the potential and have launched initiatives: Alipay and Visa.

- Alipay:

Alipay wants to enable the vast Alipay user base (1.4 bn users) to pay abroad the same way they pay in China. They call this Alipay+.

Launched in 2020.

Available across 56 markets in Asia, Europe, and the Middle East, serving 5 million merchants.

Alipay+ is neither a payments app nor a mobile wallet. The product is still Alipay.

- Visa:

A couple of days ago Visa announced a collaboration with QR payment providers to enable cross border payments across Asia Pacific.

Consumers will be able to use their Digital Wallets to (scan and) pay with POS QR-codes when traveling abroad.

In April 2023 Visa announced Visa+, an interoperability initiative to enable the sending and receiving of money across (different) digital platforms.

With Visa+ Visa wants to become the connecting infrastructure layer in the world of digital wallets and P2P apps. Just like it does for cards today.

Cleverly enough, Visa+ does not require a Visa card; only setting up (once) a personalized payment address that will, in turn, connect to the digital wallets.

What these initiatives have in common (besides the +):

They both want to build a xborder partnership infrastructure (with local players) in order to connect local merchants with consumers.

Neither is building a new product. It’s all about setting up an overarching connecting set-up.

They both use their vast ecosystems as a springboard, but both want to go far beyond.

QR code payments are a central focus.

No intervention on the customer relationship side, which remains with the local players.

Lots of services on top (i.e. marketing, settlement) to increase appeal and simplicity.

Who do you think is next?

Guest post by Panag Kriaris

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA