- Published on

The US is joining, at last, the Open Banking game.

- Authors

- Name

- AbnAsia.org

- @steven_n_t

So far, the US has refrained from introducing OB regulation, leaving it up to the market to sort out.

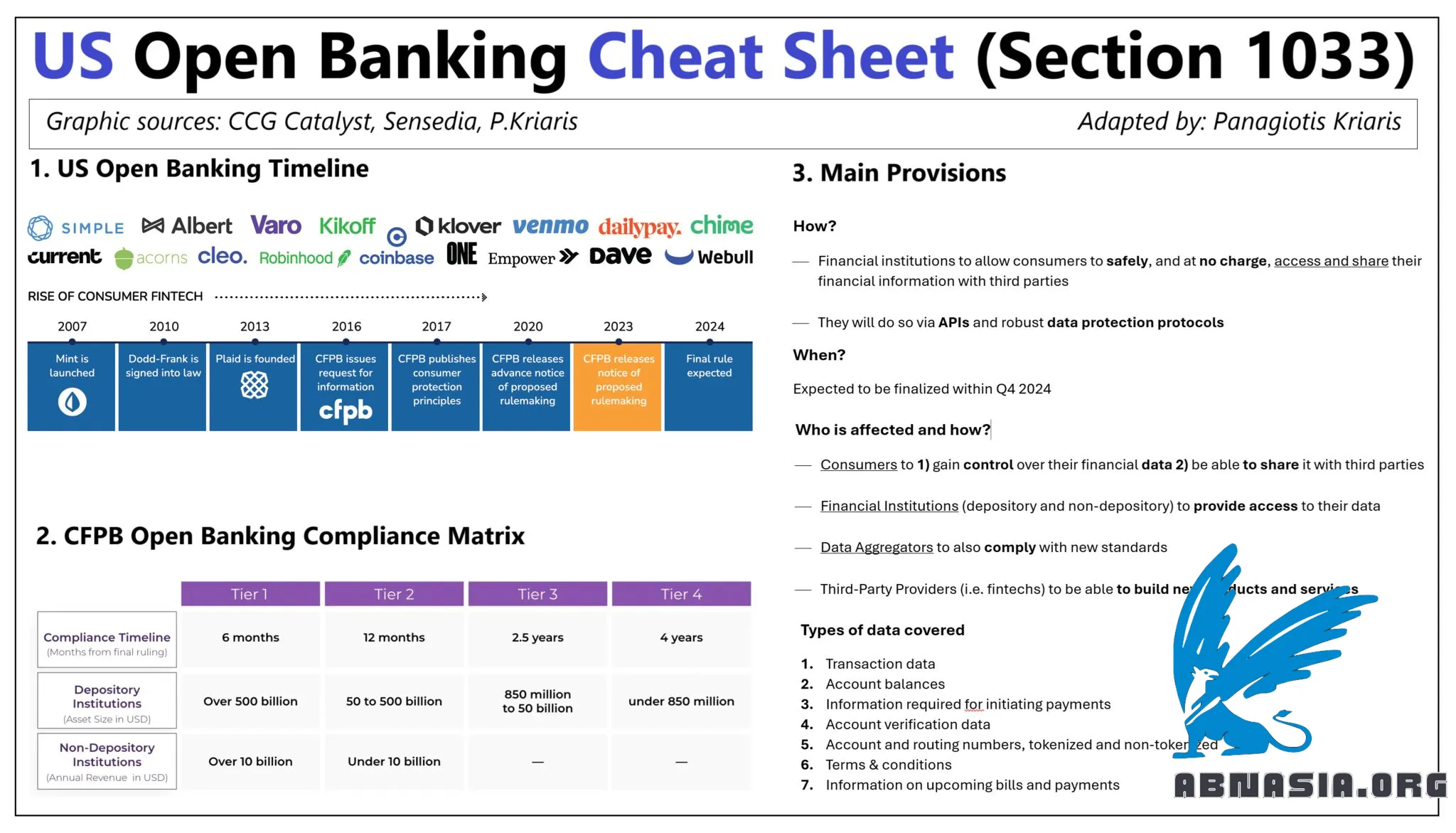

The US is joining, at last, the Open Banking game. Via regulation, despite being market driven for years. Let's see why.

So far, the US has refrained from introducing OB regulation, leaving it up to the market to sort out. A player called Plaid did exactly that: starting in 2013 it managed to build external APIs to thousands of banks and credit unions covering the entire market.

However, only 50% of third-party data access is currently done via APIs, with screen-scraping being very popular.

The Consumer Financial Protection Bureau (CFPB), which is a federal government regulator established in 2011 as part of the Dodd-Frank Act, is about to launch OB regulation.

If you come across Section 1033 of the Dodd-Frank Act, then that's the OB rule.

But why?

I have summarized 6 main goals:

accelerate the shift to open banking

get rid of inefficient data sharing (screen- scraping)

boost financial data rights

foster innovation

increase competition

enhance banking transparency

How will they do it?

Financial institutions to allow consumers to safely, and at no charge, access and share their financial information with third parties

They will do so via APIs (that have become the connecting glue for FS of all kinds) and robust data protection protocols

When?

Months in the making, the rule is expected to be finalized within Q4 2024.

Who is affected and how?

Consumers to 1) gain control over their financial data 2) be able to share it with third-party apps and services

Financial Institutions (depository and non-depository) to provide access to their data

Data Aggregators to also comply with new standards

Third-Party Providers like fintechs to be able to build new products and services based on the data access

Types of data covered

Transactional data

Account balances

Information required for initiating payments, including ETFs, prepaid accounts, gift cards and gift certificates

Account verification data: name, address, email, phone number

Account and routing numbers, tokenized and non-tokenized

Terms & Conditions: fees, interest rates, rewards terms and overdraft options

Information on upcoming bills and payments

Roll-out

Consumer-authorized third parties will have to comply within 60 days

For financial institutions a tiered approach will be followed, depending on their size (4 tiers)

Implications

On the one hand banks will have to comply with lots of obligations: APIs, developer portals, stronger data protection, consent and data transparency mechanisms, identity and authorization tools

On the other hand, OB can be a significant opportunity, also for banks to improve their offerings and position themselves closer to their customers (i.e. faster onboarding, better UX, customer dashboards, improved loan origination decisioning)

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA