- Published on

Visa vs. Mastercard vs. American Express

- Authors

- Name

- AbnAsia.org

- @steven_n_t

Visa, Mastercard, and American Express are the dominant players in the global payments industry, but they operate differently.

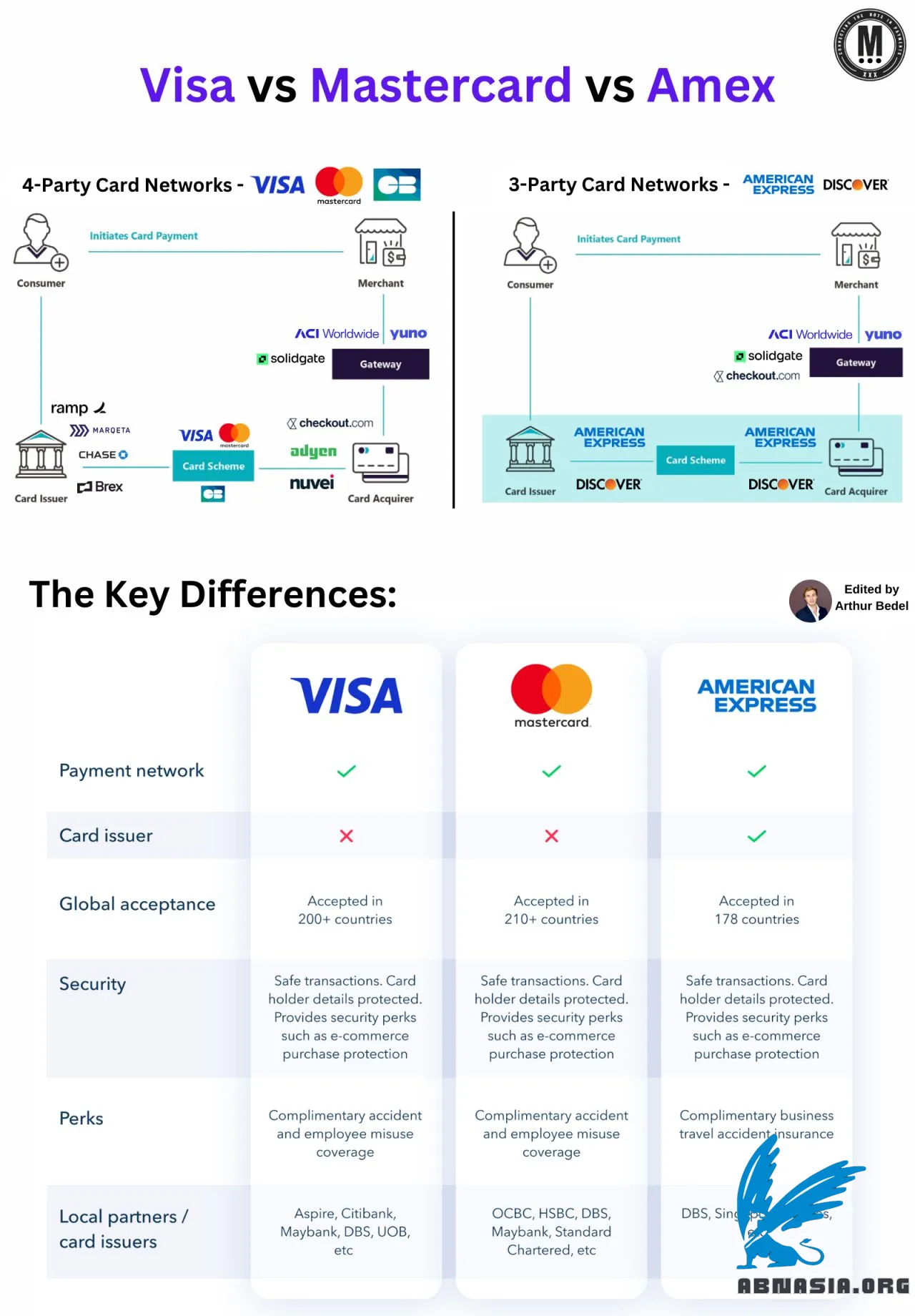

Card Payment Models:

4-Party Card Network (Visa, Mastercard, GIE Cartes Bancaires):

This model involves four key players: consumers, issuers, merchants, and acquirers. Merchants interact with customers and acquirers, while the card networks act as intermediaries.

3-Party Card Network (American Express, Discover Financial Services):

In this model, a single entity handles the roles of issuer, acquirer, and network. Merchants pay a single fee, which is often higher compared to the 4-party model.

Authorization Process at Point of Sale (4-Party vs. 3-Party Model)

4-Party Model:

The issuing bank provides a debit or credit card to the customer.

The customer swipes the card at the Point of Sale (POS) terminal to make a purchase.

The POS sends the transaction to the acquirer that owns the terminal, sharing a token.

The acquirer forwards the transaction to the card network, which passes it to the issuer for approval.

If approved, the issuer holds the funds. The approval or rejection is sent back to the acquirer and POS, and the funds are transferred.

3-Party Model:

The first three steps are the same as the 4-party model.

American Express or Discover handles all roles (acquirer, issuer, and network), making the process more efficient in a closed-loop system.

Recently, these networks have partnered with other issuers and acquirers to expand their reach.

Approval or rejection is sent back to the acquirer and POS, and funds are transferred.

Key Numbers:

In 2023, U.S. merchants paid around $224 billion in fees for card payments (including interchange, network, and processor fees).

U.S. merchants could have saved $49 billion in 2023 if fees were at 2009 levels.

In Europe, 45% of the Merchant Discount Rate (MDR) is due to interchange fees.

Key Differences:

Visa and Mastercard are payment networks, not issuers. They partner with banks and financial institutions to offer credit, debit, and prepaid cards.

Both Visa and Mastercard are accepted in over 200 countries, but their rewards and offers vary depending on the issuer.

American Express acts as both a card issuer and a payment network, giving it more control over customer service and rewards. This often makes it a premium choice.

While American Express is accepted at fewer locations than Visa and Mastercard, it offers exclusive perks to its users.

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA