- Published on

Buy-Now-Pay-Later

- Authors

- Name

- AbnAsia.org

- @steven_n_t

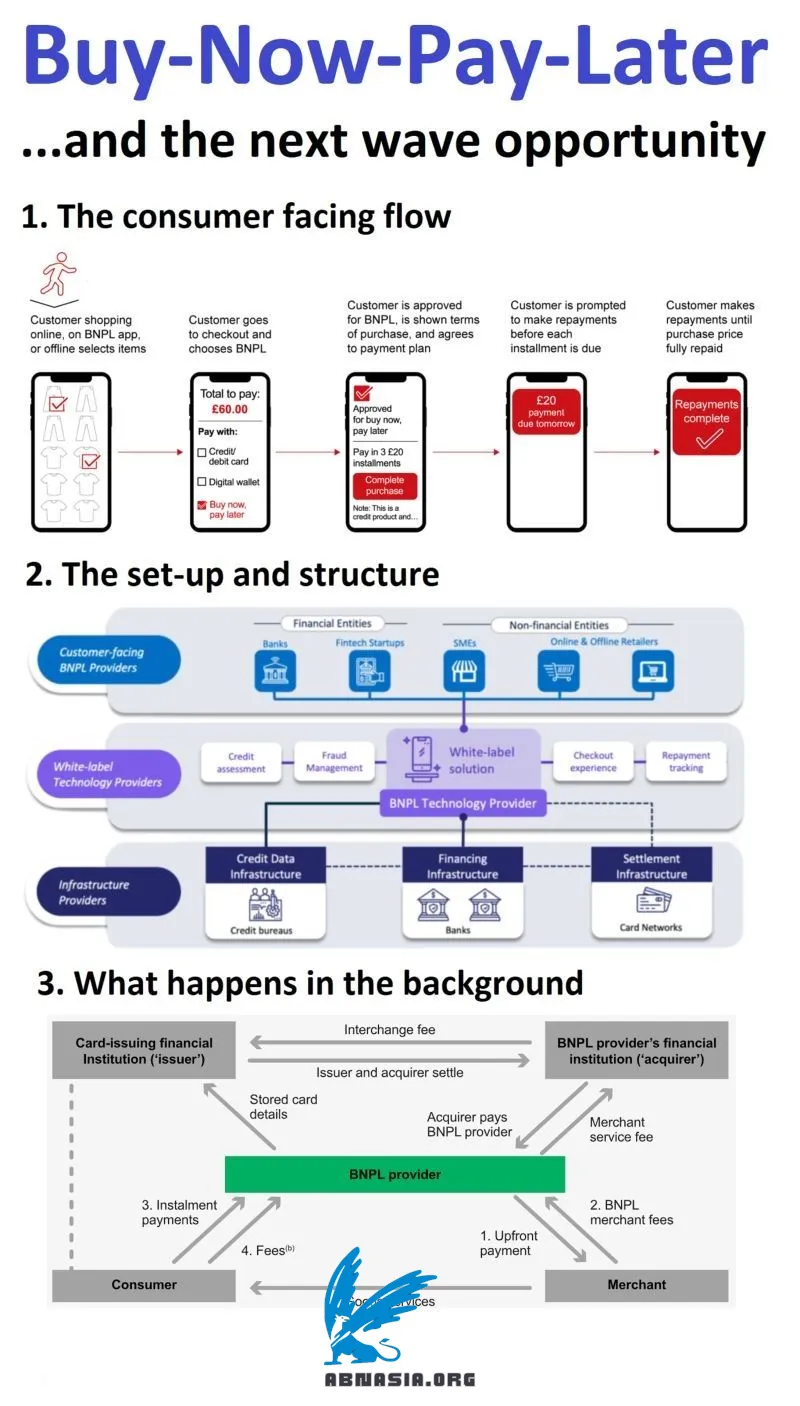

Buy-Now-Pay-Later (BNPL) owes its spectacular success to its ability to build customer trust and loyalty through seamless, embedded customer experiences.

Its transition to the next maturity level brings implications far beyond the original approach. Let’s take a look.

Amidst the increasing dominance of ecommerce and the rise of digital wallets and alternative payment methods, BNPL has established itself as an indispensable element of any payments offering.

However, the macro environment (low interest rates, growth cycle) that boosted its growth in recent years, has been the one to trigger the reverse course with high losses, plummeting valuations and even failures for several BNPL players around the globe.

Despite all that, the following needs to be considered:

— BNPL currently accounts for just over 2% of global e-commerce ($8.5 trillion in 2026 based on Worldpay) and less than 1% of the POS transaction value globally (2021 figures). These figures are estimated to double over the next few years, and they indicate that despite PayLater’s remarkable growth, it still represents a tiny pool of the global market potential.

— BNPL has a less-known white-label approach in juxtaposition to the branded version that became synonymous with its rise. Players representing this model have very attractive margins, normally support the end-to-end lifecycle (from communication to late payments) and can offer a high degree of customization.

— Customers across the globe – and especially the younger generations and clients in specific verticals such as fashion – have become so much used to the model, that a lack of the offering puts providers and merchants automatically out of the market.

At the same time several changes are taking place:

— The space is becoming increasingly commoditized with pricing and margins coming under pressure.

— Players such as Klarna that found success and became synonymous with BNPL are moving away from sole BNPL into an ecosystem approach to become a one-stop ecommerce facilitator.

— Santander, one of Europe’s biggest banks, has made a big strategy bet on BNPL by launching its own BNPL offering (Zinia) across Europe in an effort to compete with Fintechs.

— Apple has launched its own Apple Pay Later service.

— All the big players from PayPal to Square to Amazon to Discover to Visa and Mastercard are already in the game.

Going forward 4 trends will be underpinning BNPL’s transformation: 1) its transition from BNPL 1.0, a somewhat stand-alone proposition, to BNPL 2.0, where it finds its way to wider ecosystems’ offerings as a credible alternative to an increasingly multi-polar payments infrastructure 2) the widening competition that includes fintechs, retailers, bigtechs, technology companies and infrastructure providers

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA