- Published on

The $290 billion revenue opportunity

- Authors

- Name

- AbnAsia.org

- @steven_n_t

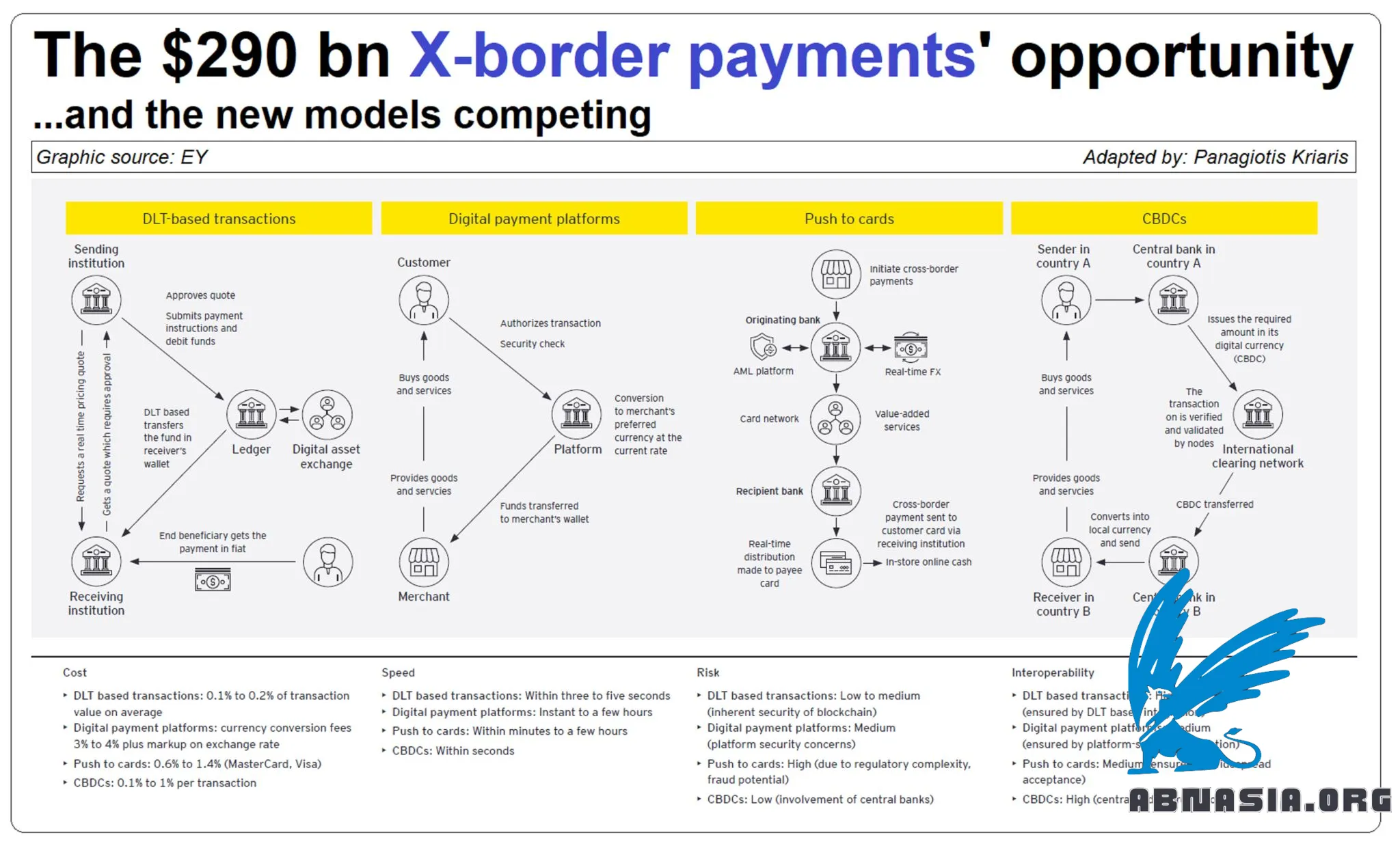

Cross-border payments are a huge, $290 billion revenue opportunity. Mostly untapped, attracting growing attention and competition. Who is winning? Lets take a look.

Compared to domestic payments, cross-border payments are notoriously more inefficient with high costs, limited transparency and slow response times. Legacy technology, complex processes and outdated data formats are some of the main culprits.

The numbers:

EY estimates total global cross-border payment flows will reach $290 trillion by 2030

Mckinsey says they are a $290 billion revenue opportunity

OliverWyman and JP. Morgan calculated that global corporates move nearly 120 billion per annum

The structure (EY data):

B2B remains the primary driver of cross-border revenue (70%+ of total)

Consumer categories carry higher margins and are growing faster (i.e. C2C)

B2B e-commerce is one of the fastest-growing

A number of players and setups, new and existing, are competing in this game:

SWIFT sits behind the correspondent banking model managing since 1973 the vast majority of B2B cross-border payments handled by banks

Blockchain. Players such as fintech startup Ripple have tried to attack the market with a decentralized infrastructure, but their volumes so far have not moved the needle in any significant way. SWIFT itself has recently been experimenting with blockchain on tokenized assets

Players with an own, end-to-end infrastructure around the globe such as Western Union and MoneyGram, servicing mainly the retail - remittance side

fintech challengers, trying to find creative, new approaches to existing pain points, such as TransferWise (now Wise) that is using a network of local bank accounts to bypass SWIFT

The big schemes, Visa and Mastercard, have launched push payment schemes (Visa Direct , Mastercard Send) using existing rails and partnered with many market-leading players in the field (i.e. Visa with WU, Mastercard with Paysend) to launch an additional pay-out solution next to existing capabilities

Central Banks launching CDBCs and building multi-currency Central Bank Digital Currency (mCBDC) networks that can work across countries, currencies, and payment systems

Cross-border payments operate on technology and infrastructure created decades ago to service a model that has little to do with today's needs. Replacing something like this on a global scale is the big challenge and the main reason why most of the innovation so far has focused on non-revolutionary solutions (i.e. creating work-arounds or adding layers). The opportunity is still up for grabs. And it's a huge one.

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA